Fintech is a combined word for Finance and Technology and its application. When technology was used to streamline and digitize traditional financial services the Fintech industry was germinated – or it can be termed as usage of technology to disrupt the financial industry and to improve customer services. It is an integration of internet technology and speeding up the financial services of depositing checks, money transactions, paying bills and more.

India’s fintech industry has rapidly evolved, positioning itself as a global fintech leader within the last decade. From pioneering the Unified Payments Interface (UPI) that transformed digital payments to the ascent of robo-advisors and peer-to-peer lending platforms, India’s fintech sector epitomizes ingenuity, attracting worldwide attention.

Here is a quick elaboration of components of the Fintech industry.

Categories in Fintech

| Category | Description |

|

Fintech Banks |

Simplify traditional banking tasks such as account opening, funding, and fraud prevention. Neo banks offer flexible checking, high-yield savings, and secured credit cards without customary fees. |

|

Digital Payments |

Cashless payments have surged, with payment apps and services leveraging direct bank transfers for transactions and user authentication. |

| Personal Financial Management (PFM) | PFM apps connect various accounts into a single dashboard, enabling data-driven decisions and budget management. |

|

Wealth Management |

Fintech solutions support financial advisors and wealth management platforms by consolidating external account data, enhancing asset growth, and providing comprehensive financial guidance. |

|

Fintech Lenders |

Use technology to simplify the lending process, address challenges in gathering accurate applicant information, and facilitate bank account connections for loan transactions. Offer consumer-friendly loan options and introduce innovations like peer-to-peer loans. |

|

Embedded Finance |

Involves seamlessly integrating financial services within everyday experiences through non-financial products and services. |

Market Overview

The global FinTech industry has been marked by a mixture of optimism and caution in recent times. The first half of 2022 witnessed a slowdown in FinTech investments due to complex interplay of factors. Greater regulatory oversight, changing customer behaviours, ongoing macroeconomic uncertainties, and geopolitical disturbances have collectively contributed to this muted growth. However, it’s important to note that the FinTech sector managed to thrive during the pandemic-induced disruptions in 2020, setting the stage for further expansion.

As of 2021, the Indian FinTech industry boasted a substantial market size of $50 billion, signifying its remarkable growth and significance in the financial landscape. What’s even more impressive is the projected trajectory of this sector, with estimates indicating that it is set to triple in size to reach approximately $150 billion by the year 2025. This astounding growth rate is exemplified by a compound annual growth rate (CAGR) of 31.6%.

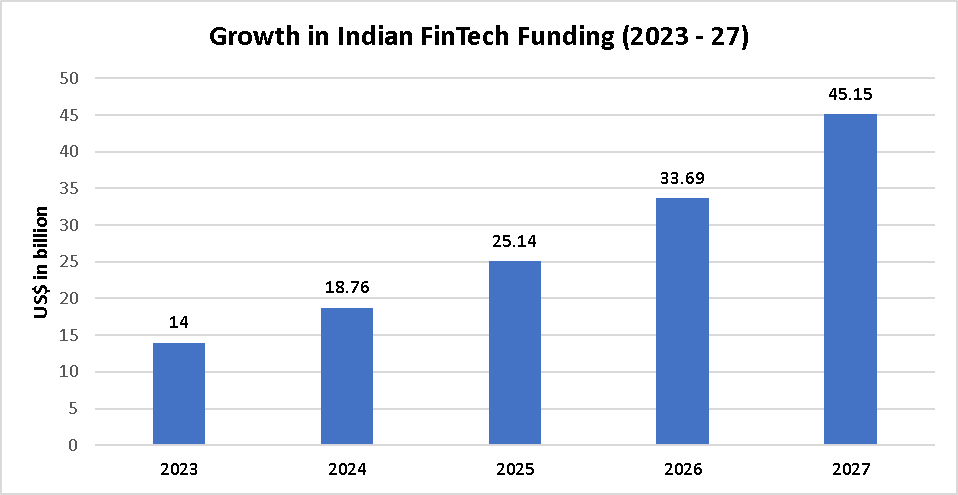

As of July 2022, India boasted an impressive number of over 7,300 FinTech startups, excluding those that were acquired or ceased operations. The total volume of FinTech funding in India reached approximately US$30.2 billion by June 2022, with an impressive 35% of these funds raised in just the past sixteen months. The year 2021 stood out as a milestone, with FinTech funding surging to a remarkable US$7.8 billion. By this assessment the fintech funding is expected to grow at a CAGR of 34% from 2023-2027.

Industry Key players

| Company | Description | Fundings | Lead Investors | Revenue |

| InCred

|

A financial services platform that leverages technology and data-science to make lending quick and easy. | US$ 357.31 million | Paragon Partners, FMO and IDFC and Saumya Mittal (angel investors) | US$63.34 million FY 2022-23. |

| Paytm Wallet: one97 Communications) | A digital payments start-up that offers innovative and intuitive digital products and services for customers and merchants. | US$4.64 billion | Some of the investors are Mark Schwartz, Berkshire Hathaway, Ant Financial, Alibaba and many more. | US$965.91 million FY 2022-23 |

| BankBazaar

|

An online marketplace that simplifies the process of comparing and applying for various financial products, such as loans, credit cards, insurance, and more. | US$117 million | Amazon, Walden SKT Venture Fund, Experian Ventures, Peak XV Partners | US$19.34 million FY 2022-23 |

| Policy Bazaar

|

A one stop destination online for all type of insurance products. It offers various insurance such as term insurance, investment plans, health Insurance, motor insurance, other insurance, business insurances and many more. | US$800.1 million | Intel, Bay capital, Tiger Global Management and Arjun Sharma. | US$96.26 million FY 2022-23

|

| LendingKart Technologies | A non-banking financial company (NBFC) that streamlines credit access by evaluating credit risk based on present cash flow rather than old vendor records. | US$$303.6 million | Fullerton Financial Holdings, Bertelsmann India Investments, India Quotient | US$99.61 million FY 2022-23 |

Investment in Indian FinTech

In the first half of 2023, the Indian fintech industry saw a significant decline in funding, with a 67% drop compared to the same period in the previous year. Despite this, the sector managed to secure $1.4 billion in total funding, only experiencing a marginal 6% decrease from the second half of 2022.

The funding dynamics within H1 2023 were noteworthy. The first quarter secured an impressive $1.18 billion, accounting for 84% of the funds garnered in the entire first half of the year. However, the subsequent quarter saw a significant funding slump, marking the lowest funding quarter since 2021.

Challenges and Opportunities

- Unicorn Growth: Despite seven funding rounds exceeding $100 million, no new unicorns emerged during this period, signaling changes in startup valuations and investor sentiment.

- Exit Strategies: The absence of new Initial Public Offerings (IPOs) in H1 2023 and an increase in acquisitions suggest potential shifts in exit strategies and sector consolidation.

- Thriving Segments: Payment, alternative lending, and internet-first insurance platforms performed well, with payment startups claiming 55% of total funding. This surge in funding in the payment sector indicates both domestic and global growth.

- Investor Landscape: Investors varied in their stages of interest, with different firms leading seed-stage, early-stage, and late-stage investments, reflecting changing perceptions of risk and opportunity within the fintech sector.

- Bengaluru’s Dominance: Bengaluru raised a substantial $949 million in H1 2023, surpassing other cities in India by a significant margin, highlighting its position as a fintech hub.

The funding decline was attributed to several factors, including a significant downturn in early-stage investments (an 81% drop compared to H1 2022), a 38% decrease in seed-stage funding, and a 62% decrease in late-stage funding compared to the previous year.

Recent Trends and Growth drivers

The Indian fintech landscape is evolving rapidly, shaped by several key trends. The surge in digital adoption, driven by the pandemic, has catapulted the industry into new realms. Fintech firms are leveraging ecosystem banking, diversifying into alternative investments, and expanding horizontally to ensure sustainable growth.

Here are some of the recent trends in Indian Fintech Industry.

- Digital Adoption Surge: Rapid growth driven by increased digital adoption across a range of financial services, including mobile payments and online investing.

- Pandemic-Driven Acceleration: The COVID-19 pandemic unexpectedly propelled fintech growth as lockdowns and distancing measures led to greater reliance on digital financial tools.

- Ecosystem Banking: Fintech companies are integrating financial services into existing ecosystems (e.g., e-commerce, super apps), enhancing user experience and transaction convenience.

- Alternative Investments: Fintech firms are seizing opportunities amidst equity market slowdowns by offering diversified investment options like peer-to-peer lending and robo-advisory services.

- Horizontal Expansion: Fintechs are broadening their services, including payments and lending, to enhance profitability and ensure sustainable growth.

- InsurTech Innovation: A surge in innovation within insurance technology (InsurTech), resulting in new insurance products and distribution channels tailored to consumer needs.

- Nedbank Partnerships: Neo banks are collaborating with fintech companies to provide highly personalized financial products, catering to specific customer segments.

Some of the industry’s key growth drivers include:

- Regulatory Support: Favorable government policies, including the Unified Payment Interface (UPI) and the Digital India initiative, promote digital payments and financial inclusion. Initiatives like the regulatory sandbox by the Reserve Bank of India (RBI) create a conducive regulatory environment for fintech innovation.

- Growing Middle Class: A burgeoning middle class with increased disposable income presents a substantial market for fintech. Fintech firms are offering tailored products and services, such as digital insurance and investment platforms, to cater to this expanding consumer base.

- Innovation and Technology: Fintech companies in India are leveraging cutting-edge technologies like artificial intelligence (AI), machine learning (ML), and blockchain to disrupt traditional financial services. For instance, AI and ML are used for credit assessment, extending financial services to underserved individuals and SMEs.

- Partnerships and Collaborations: Fintech firms are partnering with traditional financial institutions to broaden their service offerings. Collaborations like Paytm’s partnership with ICICI Bank and PhonePe’s tie-up with Bajaj Finserv enable them to offer a wider range of financial products.

- Financial Inclusion: Fintech is promoting financial inclusion, particularly in rural areas with limited access to traditional banking services. Digital payment solutions, microfinance, and other fintech services are bridging the gap between the unbanked population and formal financial systems.

- E-commerce Growth: The booming e-commerce sector in India offers fintech opportunities in providing payment solutions and financial services to online shoppers. Fintech companies like Paytm, PhonePe, and Razorpay facilitate seamless payments for e-commerce platforms.

- Wealth Management: With the rise of the middle class, there’s a growing demand for wealth management services. Fintech firms are responding with digital investment platforms and robo-advisory services tailored to this emerging market.

- Cybersecurity Focus: As the fintech industry expands, cybersecurity becomes paramount. Fintechs are investing in advanced security measures, including biometric authentication, encryption, and fraud detection, to safeguard customer data and build trust.

Conclusion

The Indian fintech industry is experiencing dynamic growth and transformation, driven by a combination of factors. Regulatory support and government initiatives have created a favourable environment for digital finance, with technologies like AI and blockchain fuelling innovation. Partnerships with traditional financial institutions are expanding the fintech ecosystem, while a strong focus on financial inclusion is bridging gaps in underserved communities. However, as the industry flourishes, cybersecurity remains a paramount concern, prompting Fintechs to invest in robust security measures.

The Indian fintech sector is poised for continued growth, promising financial inclusion, innovation, and convenience for consumers, while also addressing challenges such as regulatory compliance and data security. With these factors, the industry is expected to exhibit CAGR of 34% in the next five years from 2023 to 2027.

DART Consulting provides business consulting through its network of Independent Consultants. Our services include preparing business plans, market research, and providing business advisory services. More details at https://www.dartconsulting.co.in/dart-consultants.html