Automobile industry remains a key pillar of the Indian economy, contributing 6% to GDP, with the components segment accounting for 2.3%. It provides direct employment to over 1.5 million people and supports millions more indirectly through its extensive value chain. India is firmly on track to become the third-largest automobile and auto components market globally by 2025.

We, DART Analysts, based on data up to 2022, indicated that the Indian Automobiles & Auto Components Sector had achieved an overall industry Compound Annual Growth Rate (CAGR) of 4.8%, with projections of a 6% CAGR for the period 2023–2027. However, the subsequent analysis reveals that the sector has significantly outperformed these expectations, with the top players reported CAGR of 10% by 2025. This performance is way ahead of the corresponding industry performance 3 years back.

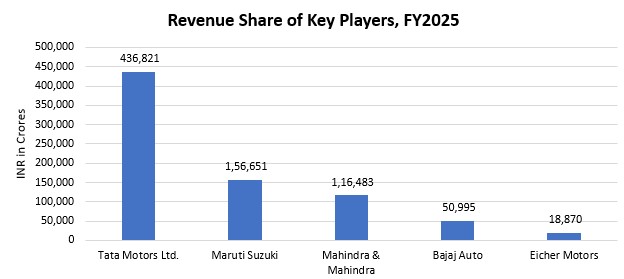

*Companies ranked based on FY2025 Revenue (highest – lowest)

This stronger-than-anticipated performance indicates the industry’s rapid post-pandemic recovery, robust domestic demand, and accelerating shift toward electric mobility and technological integration. Supported by favorable policy interventions, Production-Linked Incentive (PLI) schemes, and increased localization efforts, the sector has entered a more dynamic growth phase.

Looking ahead, overall market is now projected to sustain this momentum, growing at a 10.4% CAGR between 2026 and 2029 and the top players will continue grow. This trajectory not only reaffirms the sector’s resilience and adaptability but also highlights its strategic evolution from volume-driven expansion to value-led, innovation-driven growth.

Here is the detailed analysis of Top Players of Indian Automobiles & Auto Components Sector:

Maruti Suzuki

Maruti Suzuki India Ltd (Maruti Suzuki), a subsidiary of Suzuki Motor Corp, is an automobile manufacturing company. It manufactures and sells motor vehicles, components, and spare parts under three categories: vans, passenger cars and utility vehicles. Maruti Suzuki also offers services such as finance, insurance, accessories, and parts, driving school, leasing and fleet management. The company owns two manufacturing plants in Gurugram and Manesar. It serves customers in India, Europe, Asia, Oceania, and Latin America. Maruti Suzuki is headquartered in New Delhi, India.

Tata Motors Ltd

Tata Motors Ltd. (Tata Motors) is a leading Indian automobile manufacturer and a flagship company of the Tata Group. It designs, manufactures, and markets passenger cars, utility vehicles, trucks, buses, defense vehicles, and electric vehicles, along with related parts and accessories. The company operates across Passenger Vehicles, Commercial Vehicles, and Jaguar Land Rover (JLR) segments. Popular models include the Nexon, Punch, Harrier, and Safari, while its Nexon EV and Tiago EV make it a leader in India’s electric vehicle market. Tata Motors has manufacturing facilities across India and operations in the UK, South Korea, South Africa, and Thailand, exporting to over 125 countries. The company is headquartered in Mumbai, Maharashtra, India.

Mahindra & Mahindra

Mahindra & Mahindra Ltd (M&M), the flagship company of the Mahindra Group, is a diversified business company. It has presence in major industries such as automotive, aerospace, agri-business, aftermarket, information technology, consulting, components, clean energy, financial services, defense, real estate and infrastructure, industrial and construction equipment, two-wheelers, retail, steel, hospitality, IT services, automotive parts, aerostructures, boats, investments and logistics. It has manufacturing facilities in the US, France, Finland, India, Japan, Africa, China and Australia. The company also operates research and development centers. M&M operates in India, South Korea, Japan and Italy, besides North America. M&M is headquartered in Mumbai, Maharashtra, India.

Bajaj Auto

Bajaj Auto Ltd (Bajaj Auto) is an automotive manufacturer. The company develops, manufactures, and distributes automobiles such as two- wheeler motorcycles, three-wheeler motorcycles and commercial vehicles. The company also manufactured and markets various spare parts and accessories. Bajaj Auto offers products in entry-level, commuter and commuter deluxe, sports and super-sports lines. Bajaj Auto has manufacturing facilities in Maharashtra and Uttarakhand in India. It exports two and three wheelers in Africa, Asia Pacific, South Asia, Latin America, the Middle East and Europe. Bajaj Auto is headquartered in Pune, Maharashtra, India.

Eicher Motors

Eicher Motors Ltd (EML) is a manufacturer and marketer of commercial vehicles and motorcycles. It offers apparel, soft products, spares, and motorcycle accessories. EML also specializes in the manufacture of mid-size leisure and adventure motorcycles. The company markets its motorcycles under the brand name Royal Enfield. Its products portfolio consists of Bullet, Classic, Interceptor, Thunderbird, Continental GT and Himalayan. The company also designs, manufactures and markets dependable fuel, efficient trucks and buses. In addition, it offers medium duty trucks, heavy duty trucks, Volvo trucks, and buses. The company is also involved in manufacturing personal utility vehicles. It operates in the US, the UK, Europe, the Middle East, and South Asia. EML is headquartered in Gurugram, Haryana, India.

Industry Performance

The Indian auto component industry continues to exhibit remarkable resilience and growth. With OEM sales, exports and the aftermarket segments all growing positively, the industry clocked a turnover of Rs. 6.73 lakh crore (USD 80.2 billion) in FY25, reflecting a growth of 9.6% over the previous fiscal. Notably, the trade surplus was USD 453 million—a testament to India’s growing manufacturing competitiveness in the global market and localization initiates. The Aftermarket, estimated at Rs. 99,948 crore also witnessed a growth of 6 percent. Component supplies to OEMs in the domestic market grew by 10 percent to Rs.5.7 lakh crore.”

The industry is now witnessing a shift towards electrification, though internal combustion engine (ICE) vehicles continue to dominate. In 2024, India produced 100,000 electric cars and 900,000 electric two-wheelers, alongside 20 million two-wheelers and 5 million cars powered by ICE technology. It accounted for 2.3% of India’s GDP in FY25 and provided direct employment to over 1.5 million people, a figure expected to rise as the sector’s GDP contribution reaches 5-7% by 2026.

In FY25, India’s automobile production reached 31 million units, including 19.6 million two-wheelers, 4.3 million passenger vehicles, 0.95 million commercial vehicles, and 0.74 million three-wheelers, reflecting strong domestic demand. Domestic OEM supplies contributed 54% of the industry’s turnover (₹5.7 lakh crore / US$66.7 billion), aftermarket 10% (₹99,948 crore / US$11.6 billion), and exports 19%, marking an overall 10% year-on-year growth.

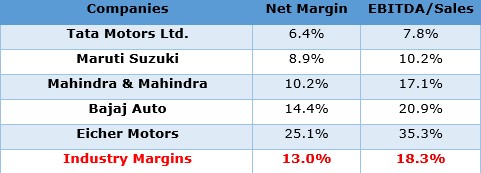

The Indian Automobiles & Auto Components Sector is already in the strong position. Globally, it is at the forefront of many segments, and the sector is gaining momentum in the global market and is also making profits. The reported margin of the industry by analysing the key players was around 7.3% by taking into consideration the last 3 years’ data. Details are as follows.

Industry Trends

- In FY25, India’s automobile production and sales reflected this momentum, with domestic sales reaching 1.96 crore two-wheelers, 43 lakh passenger vehicles, and 9.6 lakh commercial vehicles. Total vehicle exports grew by ~19% year-on-year, reaching 5.36 million units. The auto components industry turnover rose 9.6% year-on-year to ₹6.73 lakh crore (US$ 80.2 billion), underscoring sustained demand and capacity utilization.

- The SUV segment remains the primary growth driver, led by strong performance from Mahindra & Mahindra, while small-car demand has revived following favorable GST adjustments. Vehicle production continues its upward trajectory, marking a ~10.8% annual increase as of September 2025.

- The Indian automobile sector’s performance beyond initial projections is largely driven by the rapid expansion of the Electric Vehicle (EV) segment. Between 2022 and 2025, EV adoption accelerated sharply, supported by the EV Mission 2030, FAME II incentives, and PLI schemes for Advanced Chemistry Cells and Auto Components. Major OEMs such as Tata Motors, Mahindra & Mahindra, and Ola Electric expanded their EV portfolios, while new investments exceeding ₹25,000 crore (US$ 3 billion) strengthened the domestic manufacturing ecosystem.

- By FY25, EV sales surpassed 1.6 million units, growing over 45% year-on-year, with two- and three-wheelers leading adoption. This electrification wave boosted both OEM performance and component manufacturing, creating new export and localization opportunities.

- Investment activity across the sector remains robust. Between April 2000 and March 2025, the automobile industry attracted ₹3.23 lakh crore (US$ 37.85 billion) in FDI—around 5% of India’s total inflows. The auto component sector alone is expected to draw ₹25,000–30,000 crore (US$ 2.9–3.5 billion) in FY26 for capacity expansion and EV part localisation.

- On the policy front, the Government of India continues to anchor industry transformation through strategic initiatives:

-

- The Production Linked Incentive (PLI) Scheme for Automobiles and Auto Components (₹25,938 crore outlay) aims to catalyse over ₹42,500 crore in new investments between FY23 and FY27.

- The EV Mission 2030 and customs duty exemptions on machinery for lithium-ion battery manufacturing reinforce the push toward 30% electric mobility by 2030.

- The Bharat NCAP program is enhancing quality, innovation, and global standards across the component value chain.

- The Automotive Mission Plan (AMP) 2016–26 targets a US$ 300 billion turnover by 2026, with the sector contributing over 12% to India’s GDP and creating ~65 million jobs.

DART Consulting provides business consulting through its network of Independent Consultants. Our services include preparing business plans, market research, and providing business advisory services. More details at https://www.dartconsulting.