India has become one of Asia’s largest auto hubs and the market is to become a key player in global auto supply chains. The auto components industry in India has exhibited impressive growth in the past decade, both in terms of production and exports. With the ongoing growth of Indian auto industry combined with supporting government policies, the prospects of this industry are also promising. The country’s auto industry is a mix of foreign players along with local companies which are growing rapidly, and the market share of local companies is expected to improve over the coming years.

The government has been trying to encourage domestic manufacturing through various policies and incentives, which has helped boost local demand for components. This has led to companies increasing their focus on local production facilities and sourcing components from India rather than importing. The government is also making efforts to reduce logistics costs through various policy initiatives such as roll-on/roll-off (RoRo) services at ports that will help reduce overall transportation costs. The auto components industry, which accounts for 2.3% of India’s GDP currently, is set to become the 3rd largest globally by 2025.

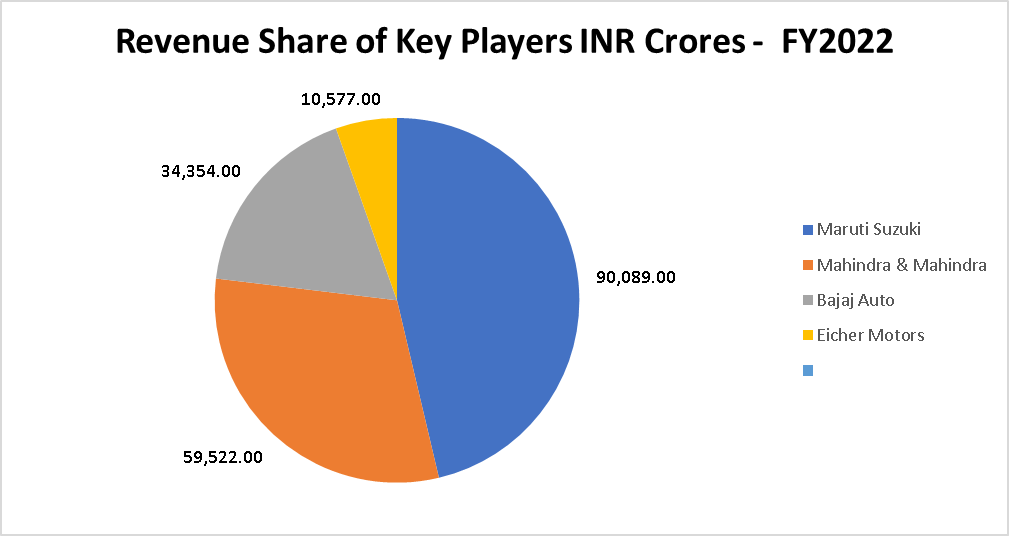

Here is a quick overview of key players in the industry.

Maruti Suzuki

Maruti Suzuki India Ltd (Maruti Suzuki), a subsidiary of Suzuki Motor Corp, is an automobile manufacturing company. It manufactures and sells motor vehicles, components, and spare parts under three categories: vans, passenger cars and utility vehicles. Maruti Suzuki also offers services such as finance, insurance, accessories, and parts, driving school, leasing and fleet management. The company owns two manufacturing plants in Gurugram and Manesar. It serves customers in India, Europe, Asia, Oceania, and Latin America. Maruti Suzuki is headquartered in New Delhi, India.

Mahindra & Mahindra

Mahindra & Mahindra Ltd (M&M), the flagship company of the Mahindra Group, is a diversified business company. It has presence in major industries such as automotive, aerospace, agri-business, aftermarket, information technology, consulting, components, clean energy, financial services, defense, real estate and infrastructure, industrial and construction equipment, two-wheelers, retail, steel, hospitality, IT services, automotive parts, aerostructures, boats, investments and logistics. It has manufacturing facilities in the US, France, Finland, India, Japan, Africa, China and Australia. The company also operates research and development centers. M&M operates in India, South Korea, Japan and Italy, besides North America. M&M is headquartered in Mumbai, Maharashtra, India.

Bajaj Auto

Bajaj Auto Ltd (Bajaj Auto) is an automotive manufacturer. The company develops, manufactures, and distributes automobiles such as two- wheeler motorcycles, three-wheeler motorcycles and commercial vehicles. The company also manufactured and markets various spare parts and accessories. Bajaj Auto offers products in entry-level, commuter and commuter deluxe, sports and super-sports lines. Bajaj Auto has manufacturing facilities in Maharashtra and Uttarakhand in India. It exports two and three wheelers in Africa, Asia Pacific, South Asia, Latin America, the Middle East and Europe. Bajaj Auto is headquartered in Pune, Maharashtra, India.

Eicher Motors

Eicher Motors Ltd (EML) is a manufacturer and marketer of commercial vehicles and motorcycles. It offers apparel, soft products, spares, and motorcycle accessories. EML also specializes in the manufacture of mid-size leisure and adventure motorcycles. The company markets its motorcycles under the brand name Royal Enfield. Its products portfolio consists of Bullet, Classic, Interceptor, Thunderbird, Continental GT and Himalayan. The company also designs, manufactures and markets dependable fuel, efficient trucks and buses. In addition, it offers medium duty trucks, heavy duty trucks, Volvo trucks, and buses. The company is also involved in manufacturing personal utility vehicles. It operates in the US, the UK, Europe, the Middle East, and South Asia. EML is headquartered in Gurugram, Haryana, India.

Industry Performance

The auto industry accounted for 2.3% of India’s GDP and provided direct employment to 1.5 million people. By 2026, the automobile component sector will contribute 5-7% of India’s GDP. The automobile component industry turnover stood at Rs. 4.20 lakh crore (US$ 56.5 billion) between April 2021-March 2022 the industry had revenue growth of 23% as compared to FY18-19. The industry is expected to grow to US$200 billion by FY26. According to ICRA, Auto ancillaries’ revenue is estimated to increase by 8-10% in FY23.

India’s auto component’s aftermarket witnessed a 15% growth from US$8.70 billion in 2020-21 to US$ 10 billion in FY22. Strong international demand and resurgence in the local original equipment and aftermarket segments are predicted to help the Indian auto component industry grow by 20-23% in FY22. In FY22, the total output of passenger vehicles, commercial vehicles, three-wheelers, two-wheelers, and quadricycles was 22,933,230 units. Automobile export is expected to grow at a CAGR of 3.05% during 2016-2026. The Government of India expects automobile sector to attract US$ 8-10 billion in local and foreign investment by 2023.

The Indian Automobiles & Auto Components Sector is already in the strong position. Globally, it is at the forefront of many segments and the sector is gaining momentum in the global market and is also making profits. The reported margin of the industry by analyzing the key players was around 10.4% by taking into consideration the last 3 years’ data. Details are as follows.

| Companies | Net Margin | EBITDA/Sales |

| Maruti Suzuki | 4.2% | 8.2% |

| Mahindra & Mahindra | 8.3% | 14.9% |

| Bajaj Auto | 14.6% | 18.8% |

| Eicher Motors | 15.0% | 24.2% |

| Industry Margins | 10.53% | 16.53% |

Industry Trends

The Covid-19 induced restrictions led to a slump in the Indian auto sector. However, the industry emerged victorious, thanks to the emergence of new technologies and innovation within the sector. To sustain the growth momentum, the industry is adopting many new trends: from increasing digital sales, expanding the used-car market to increasing safety-related measures, the sector is moving towards profitability. Rise in digital sales, SUV dominance, alternate mobility and ownership, increased acceptance of used vehicles, are some of the trends that are going to dominate the sector in 2023.

With these factors in mind, the industry is still showing huge growth potential, and here are the growth divers that is propelling the industry are:

- Global sourcing hub – At least 90 of the top 100 auto-component suppliers have presence in India. India has reduced dependence on imports with high levels of localization.

- Cost advantage – Cost in India is 10-25% lower than that of Europe and Latin America.

- Role in global value chain – 100% FDI allowed through the automatic route. Presence of auto design centres, automotive training institutes, special auto parks and virtual SEZs for auto components give India an edge.

- Geographic proximity – Geographic proximity of key automotive manufacturing countries, including ASEAN countries and South Korea are create significant opportunities for Indian auto ancillary players.

- Rise of the east – Asia emerging as a growing market backed by its cost competitiveness, rising incomes, rapid urbanization, improved infrastructure, and scope for greater vehicle penetration.

- Trade policy – Trade policy in India is favorable with nominal restrictions on import-export.

The industry is attracting major investments as follows.

- The Foreign Direct Investment (FDI) inflow into the automotive industry stood at US$33.54 billion between April 2000-June 2022.

- In November 2022, auto components maker Sona BLW precision forgings ltd. announced its plans to increase capex by Rs.1,000 crores (US$123.28 million) for its electric vehicles business.

- In March 2022, Indian and foreign automobile manufacturers took initiatives to develop hydrogen fuel cell vehicles.

The major initiatives taken by the government to promote the industry in India are as follows:

- The Government of India’s Automotive Mission Plan (AMP) 2006-26 has been instrumental in ensuring growth for the sector. The Indian automobile industry is expected to achieve a turnover of US$300 billion by 2026 by expanding at a CAGR of 15% from its current revenue of US$ 74 billion.

- In February 2022, the government received an investment proposal worth Rs.45,016 crore (US$6.04 billion) from 20 automotive companies under the PLI Auto scheme. This scheme is expected to create an incremental output of Rs.2,31,500 crore (US$31.08 billion).

- The Government of India encourages foreign investment in the automobile sector and has allowed 100% FDI under the automatic route.

In the Union Budget 2022-23, the government laid out the following initiatives:

- The government introduced a battery-swapping policy, which will allow drained batteries to be swapped with charged ones at designated charging stations, thus making EV’s more viable for potential customers.

- India’s National Highways would be expanded by 25,000 km in 2022-23 under the Prime Minister’s Gati Shakti Plan.

Through analyzing the performance of the contributing companies for the last three years, we can ascertain that the sector witnessed a compounded annual growth rate (CAGR) of 4.8% at the end of 2022. Details are as below.

| Companies | CAGR |

| Maruti Suzuki | 2.52% |

| Mahindra & Mahindra | 4.2% |

| Bajaj Auto | 7.2% |

| Eicher Motors | 5.3% |

| Industry CAGR | 4.8% |

The Indian automotive OEM industry is already in a strong position. Globally, it is at the forefront of many segments—leading in two-wheelers, segment A cars, and tractors. The industry aspires to nearly triple vehicle sales by 2026 across segments. These could be definitive tailwinds for the Indian automotive components industry, which has ambitions of its own by 2026—to double the contribution to manufacturing GDP with a four-fold growth in size and a six-fold growth in exports. The recent Union Budget announcements specific to the automotive sector have the potential to ensure that the change is fast and tectonic. The budget promises to ignite fresh demand, spur the transition to green mobility and accelerate the domestic manufacturing ecosystem. Strengthening the foundation further, the emphasis on accelerating EV adoption will further extrapolate the trajectory of growth.

With these attributes boosting the sector, the Indian Automobiles & Auto Components Sector is likely to grow 25% more than the reported growth rate and is expected to exhibit CAGR of 6% in the next five years from 2023 to 2027.

DART Consulting provides business consulting through its network of Independent Consultants. Our services include preparing business plans, market research, and providing business advisory services. More details at https://www.dartconsulting.co.in/dart-consultants.html