The India’s financial services sector is a cornerstone of its economy, encompassing banking, insurance, capital markets, and fintech. In FY 2024–25, the services sector contributed approximately 55% to India’s GDP, highlighting its central role in economic growth. The sector is valued at around USD 300 billion as of 2024, with projections indicating continued growth. Digital innovations like the Unified Payments Interface (UPI) have revolutionized financial transactions, processing over 600 million transactions daily.

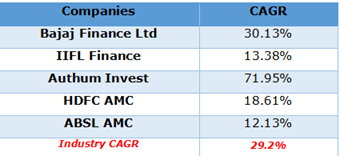

We, DART Analysts, based on data up to 2022, reported that the Indian Financial Services industry had achieved an overall Compound Annual Growth Rate (CAGR) of 31.1%, with projections of 34.2% CAGR for the period 2023–2027. The earlier analysis highlighted strong growth driven by financial inclusion, digitization, government initiatives, and diversification across NBFCs, mutual funds, insurance, and wealth management. However, the updated analysis (as of 2025) shows a moderation in growth momentum, with the industry CAGR averaging 29.2% over the period 2022–2025. This slowdown is attributed to tighter credit conditions, increased funding costs, and margin compression in lending and investment segments, along with global market volatility and regulatory tightening. Nonetheless, the sector remains resilient, supported by digital transformation, growing financial awareness, and the rise of fintech innovations, positioning it for sustainable growth in the coming years.

The performance trend suggests that while the Indian financial services industry remains structurally robust, growth has transitioned from a phase of high double-digit expansion to one of consolidation. Companies are increasingly focusing on standards and quality, strengthening governance and compliance standards, and leveraging technology-driven financial solutions to enhance efficiency and reduce risks. The sector has witnessed pressure from rising borrowing costs, regulatory tightening, and increased competition across lending and investment segments, which have collectively moderated overall profitability and growth momentum in the short term.

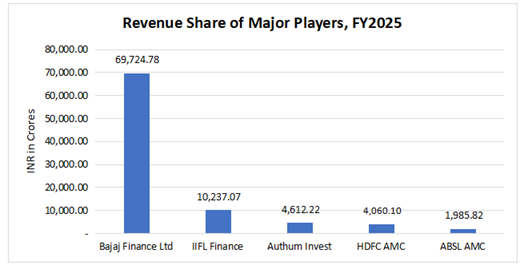

*Companies ranked based on FY2025 Revenue (highest – lowest)

Looking ahead, the Indian financial services sector is expected to stabilize and grow at a CAGR of around 22% between 2026 and 2029, slightly lower than the average growth of top-performing entities. This outlook is supported by expanding financial inclusion, the rapid adoption of digital and fintech solutions, and government initiatives such as PMJDY, GIFT City, and digital banking reforms. The industry’s evolving direction indicates a strategic transition from volume-driven credit expansion toward value-led innovation, sustainability, and technology integration, positioning India as a leading player in the global financial ecosystem in the coming decade.

Here is a quick overview of key players in the industry.

Bajaj Finance Ltd (BFL)

A subsidiary of Bajaj Finserv Ltd., Bajaj Finance Ltd. is a deposit-taking Non-Banking Financial Company (NBFC) registered with the Reserve Bank of India (RBI) and classified as an NBFC-Investment and Credit Company (NBFC-ICC). BFL engages in lending and acceptance of deposits with a diversified portfolio across retail, SMEs, commercial, and rural customers. It accepts public and corporate deposits and offers a variety of financial services including consumer lending, SME lending, commercial lending, rural lending, public and corporate deposits, partnerships, and services.

IIFL Finance

IIFL Finance Limited serves as the apex holding company of the IIFL Group, which operates a diversified financial services business. The company’s operations span credit and finance, wealth management, financial product distribution, asset management, capital market advisory, and investment banking. IIFL has been expanding its retail lending base, particularly in affordable housing and gold loans, while focusing on improving asset quality and operational efficiency. Its multi-channel approach and digital integration have positioned it as a key player in serving both individual and institutional clients.

HDFC AMC

HDFC AMC is among India’s most profitable and preferred mutual fund managers. The company offers a comprehensive suite of saving and investment options across varied asset classes to its retail and institutional customers. For an ever growing customer base that comprise individuals, families, corporates, and institutions, the company provide a one stop solution for investments that help them improve income and create wealth. The company’s Product Suite includes Equity oriented schemes/ portfolios and Debt-Oriented Schemes. Others includes Arbitrage funds, Exchange Traded Funds (ETF) and Fund of Funds (FoF).

ABSL AMC

Aditya Birla Sun Life AMC Limited ranks among the largest non-bank affiliated AMCs in India, managing diverse asset classes under its mutual fund, portfolio management, and alternate investment offerings. The company has a pan-India presence supported by subsidiaries in global financial hubs such as Singapore, Dubai, and Mauritius. ABSL AMC continues to emphasize product innovation, investor education, and digital platforms to expand its investor base and strengthen its position in the asset management sector.

Authum Invest

Authum Investment & Infrastructure Limited is a public limited NBFC engaged in investments across financial instruments, structured financing, secured lending, and equity investments in emerging businesses. The company is diversifying its portfolio by focusing on long-term wealth creation through strategic investments and financing solutions. It continues to leverage its expertise in financial structuring, risk management, and capital deployment to achieve sustainable growth in the evolving financial services landscape.

Industry Performance

The Indian financial services industry continues to be a key pillar of the nation’s economic growth, contributing significantly to GDP and employment generation. It is driven by its strong banking system, expanding NBFC network, mutual funds, insurance, and rapidly evolving fintech ecosystem. Over the past few years, the industry has demonstrated resilience amid global economic volatility, supported by sound regulatory frameworks and increasing digital adoption. Today, India is focusing on enhancing financial inclusion, promoting digital finance, and strengthening transparency and governance within the sector. By embracing innovation, technology integration, and sustainable finance practices, the industry aims to consolidate its position as one of the fastest growing and most dynamic financial markets in the world.

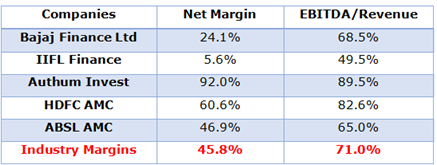

The performances of key companies in the industry give indications that the industry is profit-making and would be growing in the coming years. The reported margin of the key players was around 45%, taking into consideration the data for the last 3 years data. Details are as follows.

Industry Trends

The Indian financial services industry is undergoing a transformative phase, driven by technological innovation, strategic investments, and government initiatives. Advancements in digital infrastructure and financial inclusion efforts are reshaping how individuals and businesses access and utilize financial services. Key trends and developments highlight the sector’s growth, resilience, and future potential.

- Generative AI is enhancing customer engagement, automating workflows, and improving risk management. Financial institutions are leveraging AI for voice bots, email automation, and business intelligence, leading to productivity gains of 34% to 40% by 2030.

- The Reserve Bank of India (RBI) reported a significant increase in the FI-Index, rising from 64.2 in March 2024 to 67.0 in March 2025. This improvement reflects enhanced access, usage, and quality of financial services across the country.

- Dubai-based Emirates NBD announced a $3 billion investment to acquire a 60% stake in India’s RBL Bank, marking the largest cross-border acquisition in the country’s financial sector. This strategic move aims to bolster RBL’s growth and governance, with the deal expected to increase RBL’s net worth from $1.82 billion to $5.12 billion.

- Brookfield Asset Management announced plans to invest over $100 billion in India over the next five years, focusing on infrastructure and exploring opportunities in nuclear power projects. This commitment underscores Brookfield’s confidence in India’s growth potential.

- The government’s key financial schemes boost inclusion and support: PMJDY has opened 55.6+ crore accounts for wider banking access, APY provides pension security to 7.89 crore subscribers, and PMMY has disbursed 52+ crore loans to micro-entrepreneurs.

- The RBI is set to launch the Indian Financial Services (IFS) Cloud, developed by its subsidiary IFTAS. This initiative aims to enhance data security, privacy, and operational efficiency while ensuring compliance with data localization regulations. It will provide affordable and scalable cloud storage solutions, particularly benefiting smaller banks and Non-Banking Financial Companies (NBFCs).