On 8 Oct, a group of 136 nations covering 90 % of the world economy agreed to the OECD-G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS) after months of negotiations. The framework provides a two-pillar solution to address the tax challenges arising from the digitization and globalisation of the global economy and prevents a race by countries looking to slash tax rates to attract investment. Digitization and globalisation have had a significant effect on economies and people’s lives all over the globe, and this impact has only become stronger in the twenty-first century. Today, we may buy a product manufactured in France, packaged in China, and delivered by a British ship from a distant region of India through an American e-commerce website. These changes have posed challenges to the rules for taxing international business income that has been in place for more than a century, resulting in MNEs failing to pay their fair share of tax despite the enormous profits many of these businesses have accrued as the world has become more interconnected. This globalisation and Digitisation has caused two fundamental problems. The first is that a foreign business’s earnings could only be taxed in another nation where the foreign corporation had a physical presence under the old rules. The second issue is that most nations only tax domestic business income of MNEs but not international revenue, assuming that foreign company earnings are taxed where they are generated.

Pillar One – Re-allocation of taxing rights

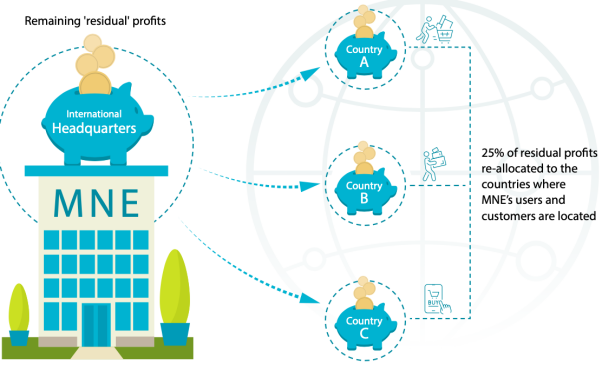

Pillar One’s goal is to shift a part of taxing rights from the jurisdiction of domicile to market jurisdictions, i.e. where the MNEs’ customers are situated. Pillar One would require sizeable multinational tech companies such as Amazon, Google, and others to pay more taxes in countries with customers or users regardless of where they operate. Taxing rights on more than USD 125 billion in earnings will be transferred to market jurisdictions under Pillar One. Under this Pillar, which will be signed in 2022 and implemented in 2023, multinational companies having a worldwide turnover of more than 20 billion euros and a pre-tax profit of more than 10% of revenue (known as supernormal profit) would be required to pay 25% of the profit before tax. This 25% will be shared among nations based on a nexus-based allocation mechanism, which is currently being negotiated.

Profits will be shifted significantly across countries as a consequence of the Pillar One plans. However, it needs measures to prevent double taxes via either a credit or exemption system. Profit shifting raises the possibility of double taxation since countries may not apply the laws in the same manner. The agreement to re-allocate earnings under Pillar One includes the elimination and suspension of Digital Services Taxes (DST), Equalisation levy and other necessary, comparable steps, putting an end to trade tensions caused by the insecurity of the international tax system. It will also offer a simpler and streamlined method to applying the arm’s length principle in certain situations, emphasising the requirements of low-capacity nations.

Pillar Two – Global Minimal Tax

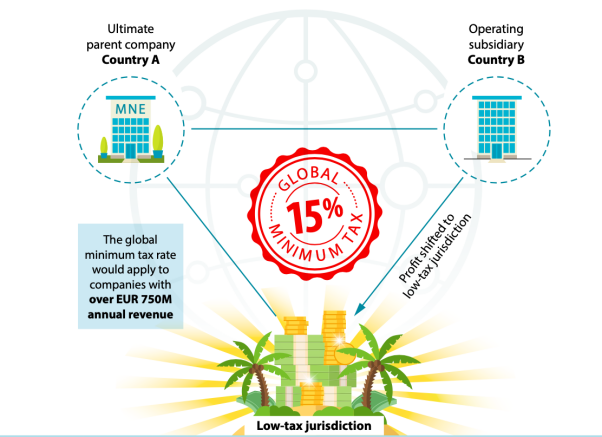

Pillar Two establishes a floor for tax competitiveness on corporate income tax by instituting a worldwide minimum corporation tax of 15%, which nations may employ to safeguard their tax bases (the GloBE rules). This implies that everywhere an MNE operates, tax competition will now be hampered by a minimum amount of taxes. The worldwide minimum tax rate would apply to multinational corporations with global revenues of 750 million euros ($868 million). Governments may continue to establish whatever local corporate tax rate they choose, but if businesses pay lower rates in one nation, their home governments could “top up” their taxes to the 15 % level, removing the benefit of transferring earnings. On the other hand, a carve-out enables nations to continue to provide tax incentives to encourage real-world economic activity, such as constructing a hotel or investing in a factory. At a rate of 15%, the global minimum tax is projected to produce about $150 billion in additional tax collections worldwide under Pillar Two. If all nations pass such legislation, the 15% corporation tax floor will be implemented in 2023.

For India, the outcome is critical due to its strong participation in OECD-led discussions. India has argued vehemently for expanded taxation powers for source or market countries. Indeed, this has been the desire of the majority of emerging nations. Because new-generation MNEs have found out how to minimise their worldwide tax incidence while earning the bulk of their revenue in developing nations. However, the new accord comes at a high cost; India must abandon its digital services tax and equalisation charge and promise to avoid introducing similar measures in the future if the global minimum tax agreement is implemented. The Indian government receives about Rs 4,000 crore in revenue from the equalisation levy. India was originally concerned that the worldwide harmonised tax of 15% would result in losing part of this income.

Nonetheless, India consented to the agreement hoping that income redistribution would benefit the country’s booming economy. While taxes are ultimately a sovereign responsibility determined by the country’s requirements and circumstances, the government is willing to join and engage in the growing global debates about company tax structure. The ball is still in the hands of the various nations. With the October Statement and the Detailed Implementation project plan in place, the Inclusive Framework moves to domestic law implementation and the negotiation, signature, and ratification of the multilateral instruments required to adjust treaty relationships among its members.

DART Consulting provides business consulting through its network of Independent Consultants. Our services include preparing business plans, market research, and providing business advisory services. More details at https://www.dartconsulting.co.in/dart-consultants.html